The Down Payment Playbook: A First-Time Buyer’s Guide

Feeling like homeownership is a distant dream? You’re not alone. Watching national news about home prices can feel incredibly discouraging, especially when you’re working hard to save for a down payment. It can make the goal of owning your own home feel like an impossible mountain to climb.

But here’s the truth from your neighbours in real estate: it is absolutely possible.

For first-time buyers right here in St. Paul and Bonnyville, or those seeking an affordable Canadian home, the path to ownership isn’t about secret tricks or lottery wins. It’s about a smart, realistic, and locally-focused plan for a simpler journey to homeownership. This isn’t generic advice from a big Toronto bank (though we happily welcome Torontonians seeking more for their money out here). This is your hyper-local playbook, built on real, current community numbers, designed to transform your dream into reality.

Let’s break down that mountain into manageable, conquerable steps. 🏡

Let’s Talk Real Numbers: What Are You Actually Saving For?

Before you can create a savings plan, you need a clear, realistic target. Vague, scary numbers are overwhelming, so let’s ground this in the reality of our local market.

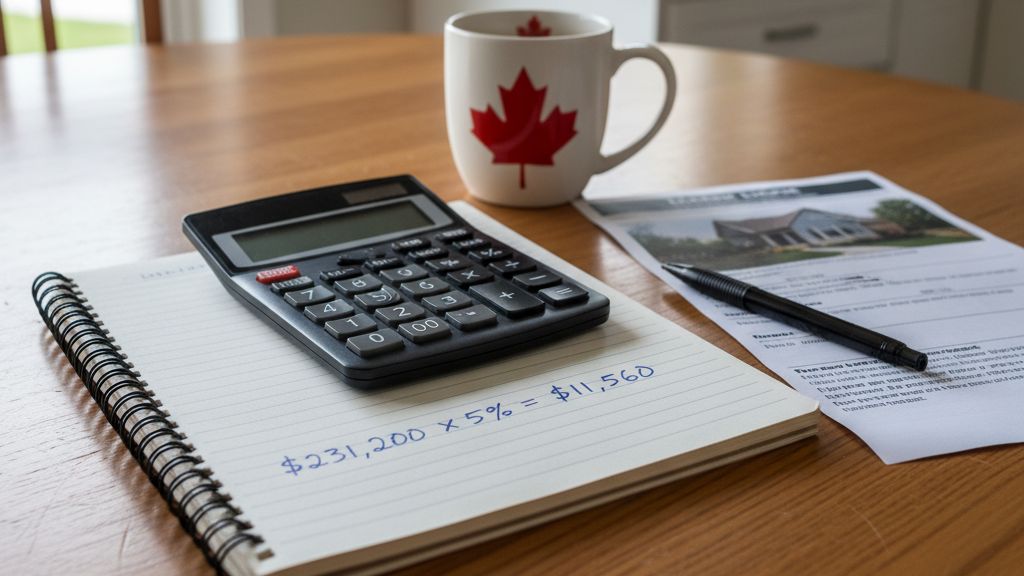

As of today, the live market data from our market reports section on our website shows the median price for a house or condo right here in the Town of St. Paul is $231,200.

This isn’t an average from across the province; it’s a real, tangible number for the type of home many first-time buyers are looking for. This is our benchmark.

In Canada, the minimum down payment is based on a tiered system:

- For homes under $500,000: You only need a minimum of 5% of the purchase price.

Let’s do the math for our St. Paul benchmark home:

$231,200 (Purchase Price) x 0.05 (5%) = $11,560

This is your minimum down payment target. Seeing it written down, you might realize it’s much less intimidating than you thought. It’s a real number you can plan for. This is your first summit to conquer.

A quick but important note: If your down payment is less than 20% of the purchase price, you’ll be required to have mortgage default insurance (often called CMHC insurance). This protects the lender, and the premium is typically added to your total mortgage amount, so it’s not a large out-of-pocket cost upfront.

Beyond the Down Payment: Budgeting for Closing Costs

This is one of the most important, and often overlooked, parts of saving for a home. The down payment is the biggest piece, but it isn’t the only cheque you’ll write. “Closing costs” are a collection of fees required to finalize the property transfer. A safe rule of thumb is to budget an additional 1.5% to 4% of the home’s purchase price.

For our $231,200 benchmark home, that means setting aside an extra $3,468 to $9,248.

Here’s what that money typically covers:

- Legal Fees: You’ll need a real estate lawyer to handle the legal paperwork, conduct a title search, and ensure the property is transferred to you correctly.

- Home Inspection: While not mandatory, a professional home inspection is highly recommended. It can save you from buying a home with major, costly issues.

- Property Appraisal: Your mortgage lender will likely require an appraisal to confirm the home’s value before they approve your financing.

- Property Tax Adjustments: The seller will have pre-paid property taxes for the year. You will need to reimburse them for the portion of the year you will own the home. This is often handled by your lawyer.

- Home Insurance: You must have proof of home insurance in place for your closing day.

- Title Insurance: This protects you and the lender from any future issues or disputes regarding the property’s title.

Saving for these costs separately from your down payment ensures you aren’t financially stressed on your closing day.

Your Savings Super-Tools: 2 Government Programs You Can’t Ignore

Saving for your down payment and closing costs is the biggest hurdle. Thankfully, the Canadian government has created two powerful, tax-advantaged programs specifically to help first-time buyers like you. Using these isn’t just a good idea; it’s essential for accelerating your journey.

1. The First Home Savings Account (FHSA): The Ultimate Savings Vehicle

Think of the FHSA as a super-powered savings account. It combines the best features of an RRSP (a tax deduction) and a TFSA (tax-free growth and withdrawal), making it the most powerful savings tool for a down payment.

- How it Works: You can contribute up to $8,000 per year, with a lifetime maximum of $40,000.

- The Tax Deduction (The “RRSP” Part): Your contributions are tax-deductible. If you are in a 25% tax bracket and contribute $8,000, you could get a tax refund of around $2,000. That refund can then go right back into your savings!

- Tax-Free Withdrawal (The “TFSA” Part): When you’re ready to buy your home, you can withdraw your contributions—and any investment growth they’ve earned—completely tax-free.

Local Impact: A couple in Bonnyville could each open an FHSA. Together, they could contribute up to $16,000 per year, getting a major combined tax deduction and building their down payment in a tax-free environment. For all the details, visit the official Government of Canada FHSA page.

2. The RRSP Home Buyers’ Plan (HBP): Borrow From Your Future Self

The Home Buyers’ Plan (HBP) allows you to borrow from your own Registered Retirement Savings Plan (RRSP) to fund your down payment.

- How it Works: You can withdraw up to $60,000 from your RRSP ($120,000 for a couple) tax-free to use towards your home purchase.

- The “Loan”: It’s an interest-free loan to yourself. You have 15 years to repay the amount back into your RRSP, starting the second year after you withdraw.

Strategic Move: Many people use the HBP to get a tax refund. You contribute to your RRSP, get the tax deduction, and then withdraw both the contribution and the refund a few months later under the HBP. To understand all the rules, check out the CRA’s page on the Home Buyers’ Plan.

The Lakeland Savings Playbook: 5 Practical Strategies That Work Here

Knowing the target is one thing; hitting it is another. Here are five realistic strategies to accelerate your savings, tailored for life in our community.

- Automate and Forget (The #1 Rule): The single most effective way to save. Set up an automatic transfer from your chequing account to your FHSA or a high-interest savings account the day after you get paid. You can’t spend what’s not there. Even $150 per paycheque is $3,900 in a year.

- The “Lakeland Lifestyle” Audit: Where does your money really go? Track your spending for one month. Is it the daily coffee run? Weekend trips to Edmonton? A boat payment? Identify one or two key areas to cut back on and redirect that cash directly to your “Future Home” fund.

- Harness the Side-Hustle: Our region’s economy often has opportunities for extra work. Whether it’s picking up an extra shift, leveraging a trade skill on the weekends, or turning a hobby into a small business on the local buy-and-sell, dedicating all income from a side-hustle to your down payment can slash your savings timeline.

- The “Lump Sum” Rule: Do you get a tax refund (especially after your FHSA/RRSP contribution!), a work bonus, or a GST credit? Earmark that money immediately for your down payment. Don’t let it get absorbed into your regular spending. This can be a massive annual boost to your savings.

- Master the “No-Spend” Lakeland Weekend: Challenge yourselves once a month. Instead of dinner out, explore what our community offers for free. A walk down the Iron Horse Trail, a fishing trip to a local lake, a St. Paul Canadiens game at the arena, a community event at the C2 Centre—it saves money and deepens your appreciation for the area you’ll soon own a piece of.

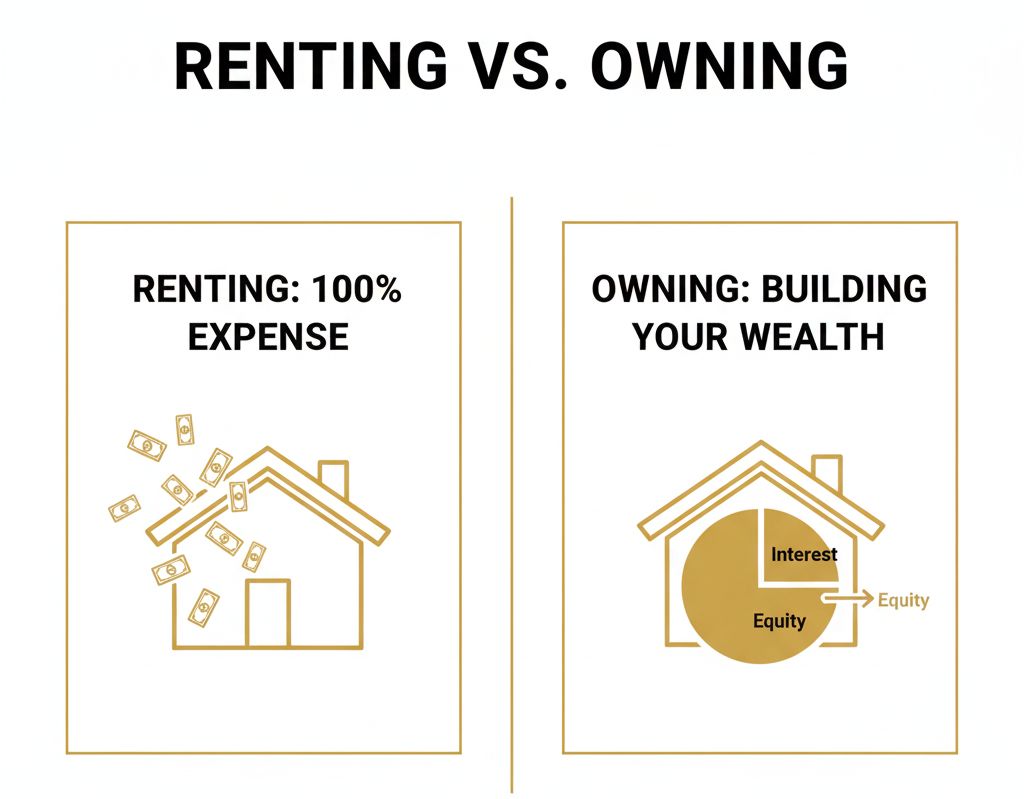

Is Renting Really Cheaper? A Local Rent vs. Buy Analysis

A common thought is, “I’m paying so much in rent, how can I save?” Let’s look at it differently. Every rent payment is 100% interest—it builds zero equity for you. Your mortgage payment, however, is part savings (equity) and part interest.

With average rents for a decent-sized home in the region often falling in the $1,200 – $1,600+ range, let’s consider the mortgage on our $231,200 benchmark home.

With today’s interest rates (and a 5% down payment), your monthly mortgage payment could be in the ballpark of $1,197-$1,500. While that might be similar to or slightly more than your rent, a significant portion of that payment—hundreds of dollars each month—is going towards paying down your own asset. You are paying yourself first.

Of course, the first step is knowing exactly what you can afford. Before you get too far, we highly recommend reading our guide on Understanding the Mortgage Pre-Approval Process.

Putting It All Together: Your 24-Month Savings Goal

Let’s imagine a couple, we’ll call them Alex and Sarah, who want to buy a home in St. Paul in two years.

- Target Down Payment: $11,560

- Monthly Savings Goal: $11,560 / 24 months = $482 per month (or $241 each)

This breaks the monumental task into a clear, achievable monthly goal. By each setting up an automatic transfer of just $241 a month into their FHSAs, they will hit their goal in two years while also getting significant tax deductions. It’s a clear, manageable plan.

Frequently Asked Questions (FAQ) for Lakeland Home Buyers

1. How much do I really need besides the down payment?

You should plan for “closing costs,” which typically range from 1.5% to 4% of the home’s purchase price. For a $260k home, that’s roughly $3,900 – $10,400 to cover legal fees, a home inspection, property tax, insurance and other administrative costs.

2. Is a 5% down payment enough, or should I save more?

5% is the minimum to get you into the market! The biggest advantage of a 20% down payment is avoiding mortgage default insurance. However, for many first-time buyers, getting into the market and starting to build equity sooner with 5% is the better financial strategy than waiting years to save up 20%.

3. What if my credit score isn’t perfect?

Your credit score is a major factor for lenders. If you know your score is low, start working on improving it now. Pay down credit card balances, make all your payments on time, and check your credit report for errors. A higher score means a better interest rate.

4. Should I use a mortgage broker or just my bank?

Both are good options. Your bank can only offer you their own products. A mortgage broker works with many different lenders to find you the best rate and terms for your specific situation. For first-time buyers, the expertise of a good broker is often invaluable.

5. What are the very first steps I should take?

Knowledge is power. Before you get too deep into saving, it’s a great idea to understand the whole journey. A perfect place to start is with these 5 Questions to Ask Before Buying Your First Home.

6. Where can I see what’s actually for sale right now?

Getting a feel for the market is a great motivator! You can see all the current homes for sale on our live Town of St. Paul Listings Page and Town of Bonnyville Listings Page.

Your Partner on the Path to Homeownership

Saving for a down payment is a marathon, not a sprint. It takes discipline, strategy, and a clear goal. But by using the powerful tools available and focusing on a realistic local target, you can and will achieve it. You are building the foundation for your future, one paycheque at a time.

Feeling inspired and ready to make a plan? 🤔

The next step is to translate this playbook into a personalized strategy.

Ready to turn this playbook into your reality? Let’s sit down for a coffee and map out a personalized homeownership plan that fits your life. No pressure, just honest advice. Contact our team at CENTURY 21 Poirier Real Estate today.

Each office is independently owned and operated.

categories

Archive

- October 2025

- September 2025

- June 2025

- March 2025

- January 2025

- October 2024

- July 2024

- May 2024

- November 2023

- June 2023

- March 2023

- November 2022

- October 2022

- July 2022

- May 2022

- March 2022

- January 2022

- December 2021

- October 2021

- August 2021

- July 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018